Generative AI burst onto the scene last November, and fueled a boom in tech stocks – a boom that effectively ended last year’s bear and sparked off this year’s market rally.

But some headwinds are starting to pile up, and some market bigwigs are predicting a crash on the horizon. Ken Griffin, the billionaire investor and founder of Citadel, is downbeat on the near term, saying, “I’d like to believe that this rally has legs, [but] I’m a bit anxious we’re in the seventh or eighth inning of this rally.”

Specifically, Griffin, who has a net worth of ~$35.4 billion, points to the Federal Reserve’s interest rate policy. For the past year and a half, the central bank has been raising rates, and he believes that the increasing effect of the rate hikes is going to outweigh the AI boom. “We’re now at the point where we’re going to see the impact of these hikes really start to play out,” he says. “We’re seeing the job market starting to weaken.”

This hasn’t caused Griffin to back away from the stock markets. Rather, he has doubled down – and more – on two of the market’s ‘tech titans,’ giants of the industry with the deep resources necessary to survive and thrive even in a recessionary environment. We’ve used the TipRanks platform to pull up the details on two of the tech giants that Griffin has bet big on recently; here they are, along with comments from the Street’s analysts.

Microsoft Corporation (MSFT)

The first stock on our list today is Microsoft, one of the best-known names in personal computing and software. The company has its hands in virtually every aspect of the home and business computer industry, and its $13 billion investment in OpenAI paid off last year, when that firm released ChatGPT and sparked off the market’s current rally.

Microsoft’s long history of both innovation and success has pushed it into the uppermost tier of publicly traded companies. Microsoft currently boasts a market cap of $2.44 trillion, and realized nearly $212 billion in total revenues in its fiscal year 2023. The company has not been resting on its laurels, however. It is using ChatGPT as the AI behind the Bing search engine, and by adding natural language capabilities to Bing is making an effort to challenge Google for market share in the search arena. Microsoft is also using AI in additional products, including its Edge web browser and its Office products, and the company’s Azure business cloud infrastructure platform is incorporating the new technology.

At the bottom line, any investment is about returns, and in its most recent quarterly report – Q4 of fiscal year 2023, which ended on June 30 – Microsoft reported a top line of $56.2 billion and non-GAAP diluted earnings of $2.69 per share. The revenue results were up more than 8% year-over-year and beat the forecast by $710 million, while the bottom line was 14 cents per share better than had been anticipated. The company’s intelligent cloud segment accounted for $24 billion of the revenue total, up 15% y/y.

For Griffin, Microsoft’s strengths are evidently clear. The billionaire stock maven added 2,041,023 shares of MSFT to his portfolio during Q2, expanding his existing holding in the stock by 150%. Griffin’s total stake in Microsoft is valued at ~$1.12 billion.

Also bullish on Microsoft is Tigress analyst Ivan Feinseth, who specifically points out the company’s large and growing AI exposure as a key point. The 5-star analyst writes, “MSFT is at the forefront of the AI revolution driven by its continued integration of increasing AI functionality, incorporating ChatGPT across all aspects of its business and product lines, which will drive the acceleration of the digital global transformation and highlights its investment opportunity. MSFT will lead the AI revolution driving change across every facet of enterprise IT and computing processes driven by the increasing need for operating efficiency, a technology-driven competitive edge, and increasing productivity and creativity. MSFT’s increasing position as a dominant AI service provider will continue to drive revenue growth and share price gains.”

These comments support Feinseth’s Buy rating on MSFT, and his $433 price target implies a 32% gain for the shares on the one-year horizon. (To watch Feinseth’s track record, click here.)

The tech titans never fail to attract attention from the Street, and Microsoft has 34 current analyst reviews on file, including 30 Buys, 3 Holds, and 1 Sell – for a Strong Buy consensus rating. The shares are priced at $328.65 with an average price target of $392.41 suggesting a 19% upside potential in the next 12 months. (See Microsoft’s stock forecast.)

Amazon (AMZN)

Next up is another instantly recognizable name, Amazon. This global leader in e-commerce got its start in the late 1990s as an online bookseller, survived the bursting of the dot.com bubble, and has since grown to become the fourth largest firm in the public markets, with a market cap of $1.44 trillion. In 2022, Amazon’s online retail operations generated some $690 billion in gross merchandise volume.

But leadership in online retail is hardly the only story here. Amazon combines practical online tech experience with enormously deep pockets, and has been developing new products to take full advantage of the emerging generative AI. These AI-powered additions to the product line include a chatbot, an image building platform, and a software code development platform. Amazon’s cloud software service, AWS, also makes extensive use of AI – and it is already generating $22 billion in annual revenue. Underneath all of this, and helping to support it, Amazon has built the brick-and-mortar physical infrastructure of its fulfillment network, with more than 541 million square feet of warehouse space.

Like Microsoft above, Amazon beat the forecasts in its last quarterly report. The results for 2Q23 showed that the company hit a top line of $134.4 billion, $3 billion more than expected and nearly 11% above the prior-year results. The revenue beat was powered by AWS, which saw 12% y/y growth and hit $22.1 billion, and the huge North American retail segment, which was up 11% y/y and totaled $82.5 billion. Amazon’s bottom line earnings, reported as an EPS of 65 cents per share, were up dramatically from the 2Q22 net loss of 20 cents per share, and beat the estimates by 31 cents.

As for Griffin, he made a strong move to acquire Amazon shares in the second quarter of this year, and bought 3,676,582 shares. This increased his AMZN holding by 258%; his exposure to Amazon now stands at $702.6 million.

Barton Crockett, from Rosenblatt Securities, is another bull when it comes to Amazon. The analyst is impressed by the company’s growing results, and believes it can leverage AI to its long-term advantage. He says in his recent note on the stock, “Our past concerns — that consensus views were too optimistic — have abated. As the business resets, with efficiency a new focus for retail, and AI an emerging driver in cloud, the risk of impending economic headwinds looks less worrying, opening the door to higher multiple consumer growth stories… Amazon is trading at an EV near 13x 2023E, well below past norms in the 20s. Meanwhile, margin improvements are accelerating EBITDA growth.”

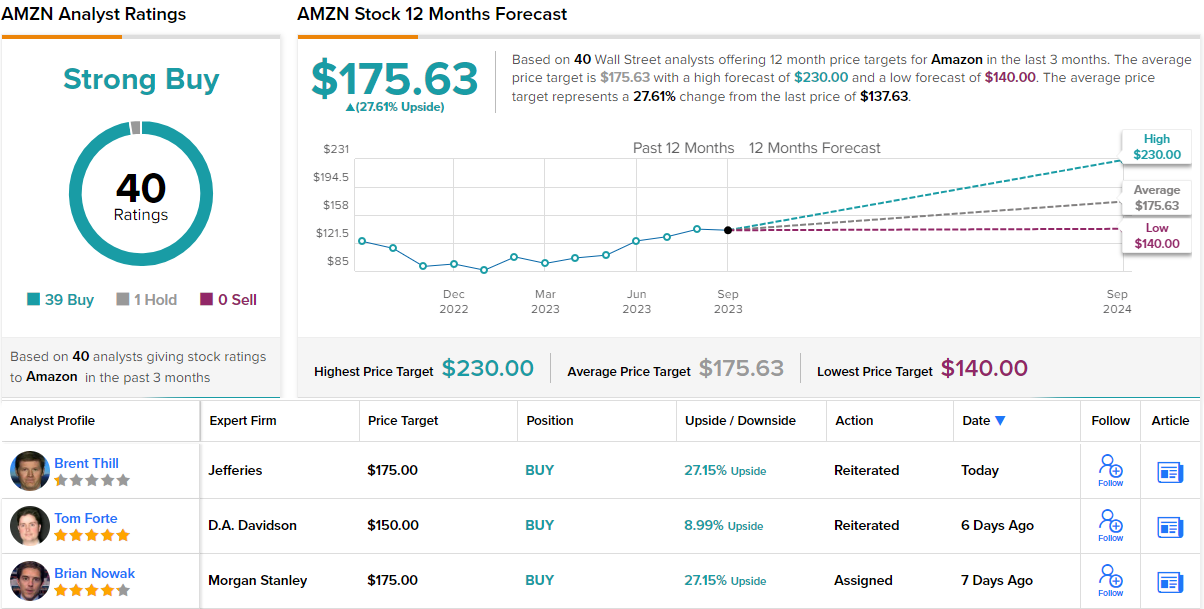

Looking ahead, Crockett gives AMZN a Buy rating with a $184 price target pointing toward a 12-month gain of 34%. (To watch Crockett’s track record, click here.)

The 40 recent analyst reviews here break down to a lopsided 39 Buys against a single Hold, backing up the Strong Buy consensus rating. Shares in Amazon are priced at $137.63, and their $175.63 average price target suggests a 28% increase on the one-year time frame. (See Amazon’s stock forecast.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Source: finance.yahoo.com