These last few weeks of 2021 have seen increased market volatility. Along with Omicron fears, the market fluctuations have come just as Wall Street is digesting the fact of a new Fed policy in the New Year, including the tightening up of monetary policy and at least one, probably more, interest rate hikes. The Fed’s easy money has been supportive for the better part of the past decade or more, and investors are rightly wondering how the market will adapt.

Looking ahead, Wedbush’s Daniel Ives is optimistic. The 5-star analyst believes that 2022 will see the tech sector push the NASDAQ to a year-end target of 19K. If he’s right, this will represent a gain of approximately 21% on the index.

A potential gain like that raises the question, where to invest? Ives sees several tech sectors as potential winners next year, including cloud computing and cybersecurity. On the cloud, Ives says, “With currently 43% of workloads on the cloud based on our estimates, we believe by the end of 2022 this figure [$1 trillion TAM] will cross the 50% threshold as more enterprises/governments head towards the cloud.” That will open up plenty of opportunities for sharp-eyed investors.

Network security is other big winner, in Ives’ view. “We believe cyber security budgets will increase 21% in 2022 which is roughly a 100 bps YoY increase from a robust 2021 based on our recent checks.” Again, this is a major increase in a segment that is already in the neighborhood of $180 billion globally. You can’t do digital without security in today’s world.

To help investors get things started, we’ve used the TipRanks platform to pull up details on three tech stocks that offer an intriguing profile: a beaten-down share price, better than 50% upside potential going forward, and a recent Buy rating from a top analyst. Not to mention, all three are rated Strong Buys by the analyst consensus. Here are the details.

Allot Ltd. (ALLT)

Let’s start with Allot, a tech company that straddles the cybersecurity and cloud computing sectors. Allot offers solutions for network intelligence, DOS protection, traffic management, and more, through a SECaaS (security as a service) model on the cloud. Allot boasts over 1 billion users, on networks in more than 100 countries.

The company has had some notable achievements to report in the press recently. At the end of November Allot announced that Poland’s leading mobile operator, Play, has entered an agreement with Allot to provide cyber threat protection for its customers – an important development, as Play has a base of 15 million subscribers. And, just recently, Allot announced that its Network Secure product in Europe blocked 1.7 million phishing attacks on Amazon.com Black Friday customers. It was a notable victory for Allot’s service.

Despite these positive developments, the company’s stock is down 41% from the peak it reached in June of this year. Even though Allot has shown steady growth in its quarterly revenues and earnings throughout the year, the company has reduced its SECaaS revenue guidance for CY21 from $8 million to $4.3 million, and lowered total company revenue projections from $150 million to $146 million.

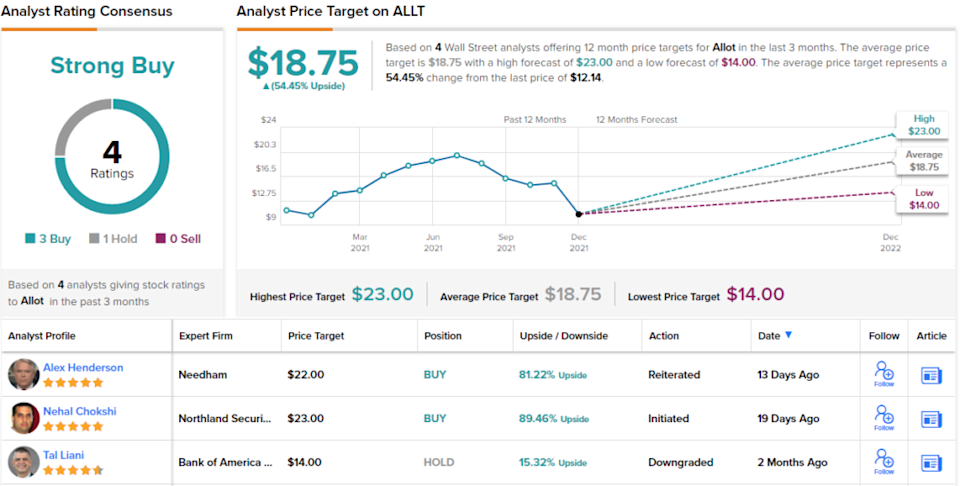

According to Nehal Chokshi, 5-star analyst from Northland Capital Markets, the depressed share price presents investors with a buy-in opportunity. He writes, “Based on our interviews of ALLT SECaaS customers located in Europe and APAC regions, we believe that CSPs are finding value from ALLT’s SECaaS technology and that end-customers of the CSPs are indeed adopting the ALLT enabled SECaaS technology. Based on input from our interviews, we analytically arrive at a $3B SECaaS revenue opportunity (see Figure 2) for ALLT.”

Chokshi puts an Outperform (Buy) rating on this stock, along with a $23 price target implying a one-year upside of 89%. (To watch Chokshi’s track record, click here.)

Turning now to the rest of the Street, Allot’s Strong Buy consensus rating is based on 4 reviews, with a 3 to 1 split between the Buys and the Hold. The shares are selling for $12.14 and their $18.75 average price target indicates room for 54% growth in the year ahead. (See Allot’s stock analysis at TipRanks.)

Airgain, Inc. (AIRG)

Next up, Airgain, lives in the cellular networking field. The company deals with solutions for wireless tech and connectivity – specifically, the antenna systems needed to connect wireless and mobile devices to the cellular networks. In addition to antenna modules, the company’s product line includes wireless modules and integrated wireless systems.

Airgain’s product lines have found wide applications, even in fields not necessarily on the cutting edge of data networking. The company’s devices are popular in IoT and fixed wireless applications, but also among first responders, public safety departments, and vehicle fleet operators. This is a diverse and wide-ranging customer base, normally a shield against hard times for sales, but Airgain has faced serious headwinds from the well-publicized supply chain disruptions – especially in semiconductor chips.

The result of those headwinds can be seen in recent revenues, which have fallen off Q2 and Q3. The third quarter top line, at $15.4 million, was down almost 11% from Q2. Earnings, which had been running positive, turned negative in the third quarter, to a loss of 11 cents per share. The company’s stock responded accordingly, and AIRG stock, which peaked in February at $28 per share, has slipped 62% from that level.

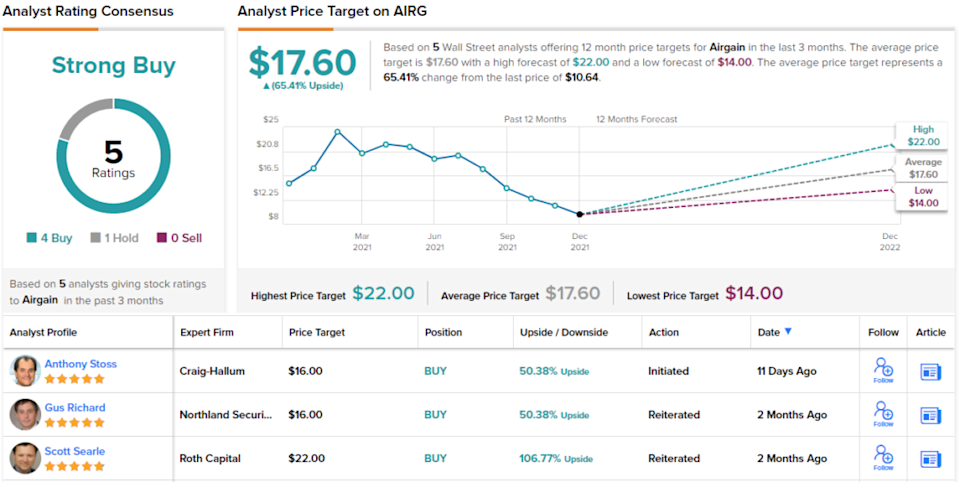

Looking at Airgain, Craig-Hallum’s 5-star analyst Anthony Stoss sees a chance to get in on the ground floor. He writes, “We believe now is the time to own AIRG as the company is poised to ride multiple tailwinds that will aid growth in existing and new products. While component shortages have affected legacy consumer business revenues in the 2HFY21, shortages are expected to begin to improve in 1Q22. We believe these supply impacts on AIRG’s legacy business have caused the market to overlook the company’s transition from a component provider to an integrated IoT wireless systems provider…. This transition will not only accelerate growth in markets with much larger TAMs, but we believe will lead to a rerate over time as AIRG’s revenue mix changes.”

In line with these comments, Stoss rates the stock as a Buy, and his $16 price target points toward an upside of 50% in 2022. (To watch Stoss’ track record, click here.)

Again, we’re looking at a company with a Strong Buy consensus rating. There are 5 reviews on file for AIRG, with a breakdown of 4 to 1 in favor of Buy over Hold. The average price target is $17.60, suggesting an upside of 65% from the 10.64 current trading price. (See Airgain’s stock analysis at TipRanks.)

Markforged Holding (MKFG)

Last on our list today is a tech company with a potentially disruptive business model. Markforged makes possible on-site production of machine tools, through a combination of software platforms and advanced, industrial-grade, 3D printers. The company’s products can move from part design to part in hand, all on the factory floor – giving manufacturers a vital advantage.

This company took advantage of the rising tide in stocks this year to go public, through a SPAC merger. The business combination with venture capitalist Kevin Hartz’ blank check firm, one, was completed in July and the MKFG ticker started trading on July 15. The deal brought Markforged a total of $361 million in gross proceeds.

In the recent third quarter report for 2021, its second such report as a public company, Markforged showed $24 million at the top line, up 53% yoy. This was accompanied by a 47% yoy increase in gross profit, to $13.7 million. The share price has been falling, some 60% from the SPAC’s peak in February – but this is not unusual; a majority of SPAC transactions see stock prices fall in their first year, before stabilizing and finding a true value.

Troy Jensen, writing on Markforged for Lake Street Capital, sees a tremendous opportunity here for this company – especially in light of supply chain disruptions. He writes, “The stock has been surprisingly weak after reporting solid results, and Markforged was the only additive company to raise 2021 revenue forecasts. We believe the current valuation represents an attractive entry point as we believe supply chain disruptions have benefitted the additive manufacturing industry in the near term. This bodes exceptionally well for Markforged given their engineering-grade printers, industrial quality materials, and innovative software make the best composite parts in the industry.”

These comments back a Buy rating, and a $14 price target implies a robust upside of 157% in the next 12 months. (To watch Jenson’s track record, click here.)

It would seem, from the aggregated reviews, that Wall Street agrees with Jensen on this one – Markforged has a unanimous Strong Buy consensus, based on 4 analyst reports. The shares are priced at $5.45 and the $10.17 average target suggests room for an 87% one-year upside. (See Markforged’s stock analysis at TipRanks.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Source: finance.yahoo.com