Oil prices appear to have found much-needed support and holding above the psychologically important level of $80/barrel just days after a surprise crude build threatened to derail the bull camp. On Tuesday, the American Petroleum Institute (API) reported another week of large crude oil inventory build at 5.213 million barrels for the week ending October 8. However, the revelation has failed to stop the oil price momentum, with WTI quoted at $81.40 per barrel on Thursday’s intraday session while Brent was changing hands at $84.10.

Oil prices are now up more than 60% in 2021, while U.S. natural gas prices have jumped 131% over the timeframe.

As usual, as energy prices go, energy stocks usually follow.

The broad energy sector benchmark, Energy Select Sector SPDR ETF (NYSEARCA:XLE), has gained 48.5% YTD while its natural gas peer, the United States Natural Gas ETF (NYSEARCA:UNG), has vaulted 112.6%.

Readers will note that oil and gas stocks have generally underperformed the commodities they track by a significant margin in the current year. The degree of underperformance becomes even more stark when you zoom out to longer timeframes.

This suggests that oil and gas stocks remain seriously undervalued and could be ready for a catch-up rally.

ESG Caps Oil and Gas Investments

Indeed, U.S. oil and gas companies are trading at less than half 2014 levels when oil prices last topped $80 per barrel, suggesting they could be seriously undervalued and ready for some catch-up trade.

Not even Big Oil has been spared, with the leader of the space, ExxonMobil (NYSE:XOM) seeing its valuation shrink from $400B in 2014 to the current $260B.

Unfortunately, experts are warning that the catch-up trade might not materialize because the fossil fuel sector has a big nemesis to contend with: the trillion-dollar ESG megatrend. There’s growing evidence that companies with low ESG scores are paying the price and increasingly being shunned by the investing community.

According to Morningstar research, ESG investments hit a record $1.65 trillion in 2020, with the world’s largest fund manager, BlackRock Inc. (NYSE:BLK), with $9 trillion in assets under management (AUM), throwing its weight behind ESG and oil and gas divestitures.

Michael Shaoul, Chairman and Chief Executive Officer of Marketfield Asset Management, has told Bloomberg TV that ESG is largely responsible for lagging oil and gas investments:

“Energy equities are nowhere close to where they were in 2014 when crude oil prices were at current levels. There are a couple very good reasons for that. One is it’s been a terrible place to be for a decade. And the other reason is the ESG pressures that a lot of institutional managers are on lead them to want to underplay investment in a lot of these areas.”

Though less frequently discussed seriously compared to Peak Oil Demand, Peak Oil Supply remains a distinct possibility over the next couple of years mainly due to serious underinvestments in oil and gas.

In the past, supply-side “peak oil” theories mostly turned out to be wrong mainly because their proponents invariably underestimated the enormity of yet-to-be-discovered resources. In more recent years, demand-side “peak oil” theory has always managed to overestimate the ability of renewable energy sources and electric vehicles to displace fossil fuels.

Then, of course, few could have foretold the explosive growth of U.S. shale that added 13 million barrels per day to global supply from just 1-2 million b/d in the space of just a decade.

It’s ironic that the shale crisis is likely to be responsible for triggering Peak Oil Supply.

In an excellent op/ed, vice chairman of IHS Markit Dan Yergin observes that it’s almost inevitable that shale output will go in reverse and decline thanks to drastic cutbacks in investment and only later recover at a slow pace. Shale oil wells decline at an exceptionally fast clip and therefore require constant drilling to replenish lost supply.

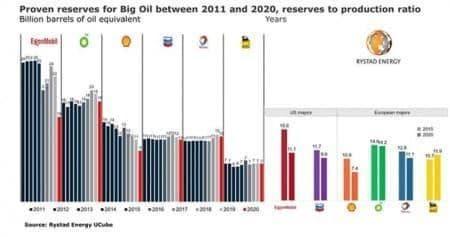

Indeed, Norway-based energy consultancy Rystad Energy recently warned that Big Oil could see its proven reserves run out in less than 15 years, thanks to produced volumes not being fully replaced with new discoveries.

According to Rystad, proven oil and gas reserves by the so-called Big Oil companies, namely ExxonMobil, BP Plc. (NYSE:BP), Shell (NYSE:RDS.A), Chevron (NYSE:CVX), Total (NYSE:TOT), and Eni S.p.A (NYSE:E) are all falling, as produced volumes are not being fully replaced with new discoveries.

Source: Oil and Gas Journal

Last year alone, massive impairment charges saw Big Oil’s proven reserves drop by 13 billion boe, good for ~15% of its stock levels in the ground. Rystad now says that the remaining reserves are set to run out in less than 15 years unless Big Oil makes more commercial discoveries quickly.

The main culprit: Rapidly shrinking exploration investments.

Global oil and gas companies cut their capex by a staggering 34% in 2020, in response to shrinking demand and investors growing weary of perennial underperformance by the sector.

The trend shows no signs of moderating: First quarter discoveries totaled 1.2 billion boe, the lowest in 7 years with successful wildcats only yielding modest-sized finds as per Rystad.

ExxonMobil, whose proven reserves shrank by 7 billion boe in 2020, or 30%, from 2019 levels, was the worst hit after major reductions in Canadian oil sands and US shale gas properties.

Shell, meanwhile, saw its proven reserves fall by 20% to 9 billion boe last year; Chevron lost 2 billion boe of proven reserves due to impairment charges while BP lost 1 boe. Only Total and Eni have avoided reductions in proven reserves over the past decade.

With public companies supplying around half of the world’s oil production, the risk of a severe oil supply crunch is very real.

Reality has already started hitting home in the U.S. shale patch.

According to the U.S. Energy Information Administration’s latest Drilling Productivity Report, the United States had 5,957 drilled but uncompleted wells (DUCs) in July 2021, the lowest for any month since November 2017 from nearly 8,900 at its 2019 peak. At this rate, shale producers will have to sharply ramp up the drilling of new wells just to maintain the current production clip.

The EIA says the sharp decline in DUCs in most major U.S. onshore oil-producing regions reflects more well completions and, at the same time, less new well drilling activity – proof that shale producers have been sticking to their pledge to drill less. Whereas the higher completion rate of more wells has been increasing oil production, especially in the Permian region, the completions have sharply lowered DUC inventories, which could limit oil production growth in the United States in the coming months.

But now, some oil executives are warning that more shale will be needed to offset normal production declines, and investors will have to accept it.

“Spending in 2022 will have to be higher just to sustain volumes enjoyed in 2021 and I think in general Wall Street is aware of that,” Nick O’Grady, chief executive at Northern Oil and Gas Inc (NOG.A), has told Reuters.

The fact of the matter is that investments in renewable energy are simply not growing fast enough to meet global energy demand, and the world will continue relying heavily on oil and gas for years, if not decades, the ongoing climate crisis notwithstanding.

By Alex Kimani for Oilprice.com

Read this article on OilPrice.com

Source: finance.yahoo.com